1. Executive summary

We are making two improvements to the way in which corporate bonds are treated in the national accounts in Blue Book 2017. The first and most significant improvement is to the way we calculate interest paid to the holders of corporate bonds. This new method has been developed as part of the wider Enhanced Financial Accounts initiative, which aims to significantly improve the information available in the UK’s sector and financial accounts. It fits within the approach recommended by Professor Sir Charles Bean’s Review of UK economic statistics of making incremental improvements to address shortcomings in the national accounts.

Our improved method increases the amount of interest paid on UK-issued corporate bonds. Some of this interest is paid between sectors of the UK economy, but a significant amount is paid to non-resident holders of corporate bonds. As a result, the improvement markedly increases the current account deficit and reduces gross national income (GNI).

The second improvement concerns the under-reporting of corporate bond repayments. The outcome results in lower net issuance (flow) of corporate bonds, with impacts on net financial borrowing from 2013 onwards. Levels of corporate bonds are unaffected by this change.

The numerical impact of these changes on important economic aggregates covering the years 1997 to 2012 can be found in the article Impact of Blue Book 2017 changes on the sector and financial accounts, 1997 to 2012 published on 19 April 2017. The impact of all the measurement improvements being made to the sector and financial accounts and balance of payments for the years 1997 to 2012 will be published on 5 June 2017, with the impacts for 2013 to 2015 published in August 2017.

Back to table of contents2. Introduction

We are publishing a series of articles that collectively explain the forthcoming improvements to the UK national accounts. This article explains two improvements we are making to the treatment of corporate bonds in Blue Book 2017:

- improvements to interest accrued

- bond redemptions

The first improvement is to the calculation of interest paid (and received) on UK corporate bonds. This improvement is the end result of internal investigations into the plausibility of the current estimates and collaborative working with the Bank of England to better measure these payments. We focus on this improvement in this article as it is by far the most significant. We set out the background, concepts and context to the changes being made, describe the new method in detail, and summarise the impacts.

The second improvement we are making is to the calculation of corporate bond flows, specifically what happens when a bond is repaid. This follows user concerns that estimates of net bond issuance have been too high in recent years.

Back to table of contents3. National Accounts concepts and economic setting

Bonds and bond interest

Bonds are a form of debt instrument issued to borrow money. In general, they are a contract to pay the holder of the bond a specified amount of money (called the “face value” or “nominal value”) on a particular date in the future (called the “maturity date”). Bonds can be purchased and sold and the price could be different to the nominal value. The current value of a bond is referred to as its market price.

Most commonly, the bond will contain an agreement to pay interest (either fixed or variable) at regular intervals to the holder of the bond, sometimes referred to as a coupon. This interest payment is a form of property income in the national accounts and investment income in the balance of payments.

Implied rates of return on bonds

In the context of this article, the rate of return is defined as the amount of interest accrued annually divided by the value of the bond. This is also sometimes referred to as a yield. For most of this article, and in particular during the description of the proposed new method, we focus on the nominal yield (which is calculated from the issue price of the bond), as opposed to the current yield (based on the market price).

The rate of return is fairly straight forward to calculate for fixed rate bonds. For other types of bond, such as “zero coupon” bonds (which pay no interest but are instead sold at a discount), this is more difficult to assess, as the return on the bond is earned through the discount unwinding over time. The rate of return concept provides a way of comparing bonds.

One important factor that influences the rate of return is the risk to the bondholder of the bond issuer defaulting on the bond; that is, not making all payments due to the bond holder. The more likely the institution is to fail to return the loaned funds, the higher the risk premium demanded by investors and the higher the rate of return at issue will be.

For fixed rate bonds, the rate of return will also reflect prevailing interest rates at the time of issuance. The rate of return on variable rate bonds, however, will reset periodically according to a particular reference rate, such as LIBOR (the London interbank offered rate). The rate of return on a bond will also be affected by the length of time from its issuance date to the date on which it matures (its original term to maturity).

We can generalise this to a collection of bonds with different maturities and different risks of default, such as those issued by a whole sector of the economy. In this case, dividing interest accrued during a year by the average1 nominal value of the bonds during the year to get an average rate of return. As this isn’t the actual rate of return on a specific investment, we refer to this as an implied rate of return. Rates of return are not published as part of the national accounts, but calculating them can be useful in determining whether payments linked to instruments (such as interest on bonds) are plausible. This is consistent with the debtor approach to estimating the implied rate of return, as it reflects the cost to the issuing institution of raising money via debt markets (the interest accrued).

When calculating implied rates of return, we must be aware of manufactured interest payments. Implied rates of return reflect the cost of servicing the bonds issued by a particular institution. Manufactured interest, on the other hand, is a payment made by an institution other than the issuer while it holds a short position on a bond. As will be discussed later, manufactured interest is present in one of the main data sources and this is factored into the method.

Bond redemptions

Most bonds are due to be repaid on a specified maturity date, although bonds can be repaid before the maturity date. Some bonds have options built into them allowing the bond issuer or holder to end the bond early. The bond issuer can also buy back their bonds on the open market before the maturity date.

Notes for: National Accounts concepts and economic setting

- The average value of assets or liabilities in a particular period is the mean of the value at the end of the particular period in question and the value at the end of the previous period.

4. Current methods

Estimating interest accrued on UK-issued corporate bonds

At present, we estimate bond interest payments using publicly available data on individual bonds from the London Stock Exchange (LSE). This process was thought to work reasonably well for fixed rate bonds, where the interest rate is often contained within the bond description. However, this information isn't always present in the LSE data, and it is much harder to establish the amount of interest accrued on variable rate bonds. In addition, the system we used to process the bonds data was fragile and lacked transparency. As part of a comprehensive review of the financial accounts undertaken as part of the Enhanced Financial Accounts initiative (the UK Flow of Funds project), it was identified that the current method gives an implied rate of return for corporate bonds that is generally lower than the rate for UK government bonds. This is shown in Figure 1.

The implied rate of return in part reflects the risk that the bond issuer defaults; that is, whether or not the holder receives the full value of the bond over its life. All other things being equal, higher rates of return imply a higher risk of default. Government bonds (“gilts” in the UK), particularly those issued by developed nations, are at low risk of default. Governments have a reliable ongoing source of income: tax revenues from their populations. If the bond is issued in the country’s own currency, they can if necessary create more to honour the bond. Corporations on the other hand have at least some risk of insolvency or illiquidity and therefore of not being able to honour their debts. While other factors such as the mix of maturity lengths of bonds in issue will also be factors, government bonds should generally have lower implied rates of return than corporate bonds.

Figure 1 shows that in the national accounts, the opposite is currently the case. As previously explained, this outcome is unusual, so we began work to investigate whether the current approach captures all interest paid. The source for government bond interest (data from the Debt Management Office) is of high quality, so attention moved to focus on corporate bond interest.

Figure 1 shows that bonds issued by the rest of the world also have relatively low implied rates of return compared with UK government bonds. However, this is a more plausible outcome than the low rate of return on corporate bonds. The “rest of the world” category includes both government and corporate bonds issued by non-resident institutions, which means it will include debt with lower risk premiums.

Figure 1: Current method implied rates of return on bonds (market prices1), 1998 to 2012

UK

Source: Office for National Statistics

Notes:

- Corporate bond values are “marked to market” using Markit iBoxx data in the National Accounts. Market prices are used in this graph as nominal rate of return cannot be calculated for rest of the world bonds using current ONS data.

Download this chart Figure 1: Current method implied rates of return on bonds (market prices^1^), 1998 to 2012

Image .csv .xlsAs part of the Enhanced Financial Accounts initiative, we have been looking for new data sources. There is currently no definitive source on corporate bond interest payments. However, data from the Bank of England allow for significantly better estimates of interest paid and received by banks and building societies, and are a means of calculating indicative rates of return for other sectors. We have worked closely with colleagues at the Bank of England on this development and we are grateful to them for their advice and support.

Improving the measurement of corporate bond repayments and net issuance

The current method for capturing bond outflows uses commercial data on bond announcements. A recent review, following a user query, identified that bond repayments were not being fully captured in the national accounts by this method. This has led to estimates of net issuance (that is, new issues less repayments) of corporate bonds that were too high. Our new method better captures bond redemptions and hence net bond issuance. Corporate bond levels and bond flows are estimated separately from each other, so this change has no impact on corporate bond levels.

Back to table of contents5. Improved methods

Estimating interest paid on UK-issued corporate bonds

In this section, we outline the improved sources and methods for estimating interest paid on corporate bonds. We are still in the process of finalising the best data source for calculating corporate bond repayments.

Sources used in estimating interest paid on UK-issued corporate bonds

The new method uses a range of sources to produce improved estimates of bond interest payments (and receipts). The sources used are:

data collected by the Bank of England’s Profit and Loss form (Form PL); this fully covers bond interest paid and received by monetary financial institutions (MFIs) – essentially, banks and (from 2008 onwards) building societies

data collected by the Bank of England’s Form A3, which was replaced by Form PL in 2004; Form A3 also collected data on interest paid and received, but only for banks

data collected by the Bank of England on their balance sheet return form (Form BT); this gives values for bonds issued by MFIs, which is important for estimating rates of return on these bonds

data collected by the Bank of England’s survey of Issuing and Paying Agents (Form IPA), which primarily tracks new issues and repayments of all UK corporate bonds but also includes some coupon payments on fixed rate bonds; Form IPA data are used to estimate implied rates of return for the main bond-issuing sectors, and to estimate manufactured interest paid by MFIs

London Stock Exchange data on corporate bonds in issue for sectors other than MFIs, particularly private non-financial corporations (PNFCs) and other financial institutions (OFIs); these data are combined with estimated rates of return to calculate interest paid by these sectors

ONS survey data on corporate bond assets held by each sector, to attribute interest received to the correct sectors

New method for estimating corporate bond interest

Calculate interest paid by MFIs, using data from Bank of England Forms PL and A3.

Estimate manufactured interest paid by MFIs, using data from Bank of England Forms PL, A3, BT and IPA.

Estimate implied rates of return for other sectors, based on the MFI rate (adjusted for manufactured interest) and data collected from the Bank of England’s Form IPA.

Calculate interest paid by other sectors, using implied rates of return and existing bond liability data, resulting in an estimate of total interest paid.

Allocate total interest to receiving sectors, using Form PL/A3 data for MFIs, and in proportion to bond assets held for other sectors.

These five stages will now be explained in more detail.

Stage 1: determine interest paid by MFIs

Interest paid by banks is taken directly from data collected from the Bank of England’s Form PL from 2004 onwards. Prior to 2004, the data are taken from the Bank of England’s Form A3.

Interest paid by building societies is taken directly from the total for building societies from the Bank of England’s Form PL, for all years available (2008 onwards). Prior to that, the existing ONS estimates have been retained. There is little difference between the Form PL data for building society interest payments and what we currently hold in the period where both are available.

Stage 2: calculate and adjust for manufactured interest paid by MFIs

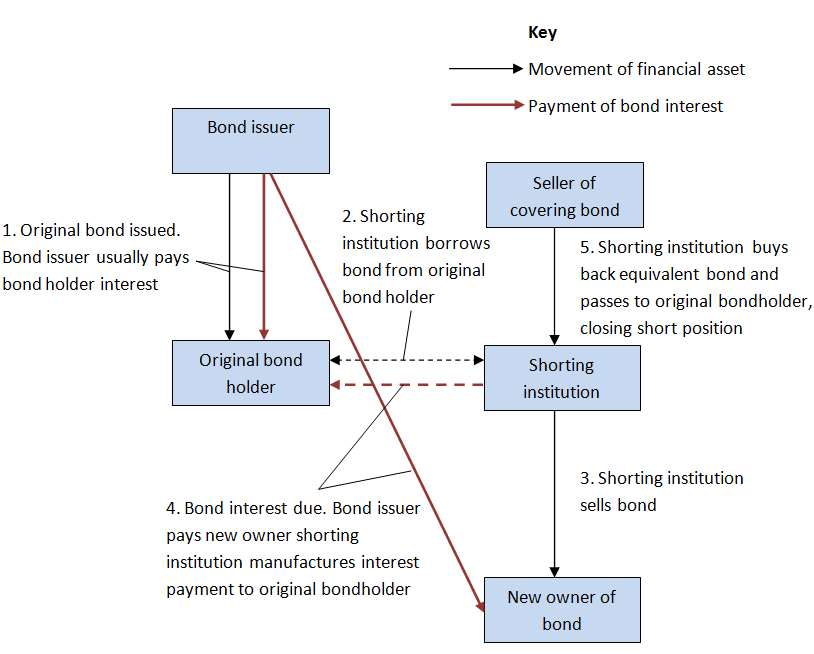

Manufactured interest arises when a bond is sold short. Shorting a bond requires the shorting institution to borrow the bond for a period of time, during which they aim to sell and then buy back an equivalent bond at a lower price. During the time the bond is borrowed, the shorting institution has to “manufacture” any due interest payments to the original holder of the bond. Figure 2 illustrates the transactions that take place when a bond is short sold.

Manufactured interest is a genuine payment by the shorting institution. However, it does not reflect interest paid on the bonds the shorting institution has itself issued, and should not contribute to the rate of return for MFI bonds calculated at the start of stage 3.

Figure 2: Transactions in bond short-selling

Source: Office for National Statistics

Download this image Figure 2: Transactions in bond short-selling

.PNG (33.9 kB){kind=link}

The Bank of England, during investigations with respondents to its Form PL, found that some respondents had been including manufactured interest payments in their survey returns. Unfortunately, it was not possible to directly quantify these payments, although the Bank of England advised that short selling activity was likely to be greater before the financial crisis than it has been since. The size of the impact has been estimated by comparing the implied rate of return on MFI-issued bonds from different sources.

First of all, we calculate the implied rate of return on bonds issued by banks by dividing interest paid as calculated in stage 1 by the average nominal value of liabilities (taken from the Bank of England’s Form BT); this implied rate of return potentially includes manufactured interest.

From 2004 onwards, we calculate the difference between this and the average blended interest rate for MFI bonds, based on data from the Bank of England’s Form IPA (see stage 3 for details on how the blended interest rate is calculated).

The presence of manufactured interest in Form PL is not the only possible source of difference between the implied rate of return calculated in the previous step and the rate derived from Form IPA data. Forms IPA, BT and PL are separate data collections by the Bank of England and some differences in the resulting implied rates of return are to be expected. The Form IPA approach additionally involves imputing rates of return for variable rate bonds. In particular, manufactured interest payments are positive and so this issue alone cannot explain the differences turning negative in 2010 (meaning the IPA implied rate of return is higher).

In the absence of further information, in periods between 1997 and 2012 where the IPA rate is lower than that derived from Forms PL and BT, it has been assumed that half of the difference is manufactured interest. Where the IPA rate is equal or higher, it has been assumed no manufactured interest has been captured by Form PL.

The estimate of manufactured interest is then subtracted from bank interest paid. In line with guidance in the International Monetary Fund (IMF) Handbook on Securities Statistics, manufactured interest is treated as negative income for the shorting MFI (see stage 5).

Stage 3: calculate implied rates of return for other sectors

This stage starts with the implied rate of return on MFI-issued bonds adjusted for manufactured interest, as described in stage 2. For each sector, we calculate a premium based on comparing the blended rates of return on bonds provided by the Bank of England, using the Form IPA data.

Form IPA data are available from 1999. However, the Bank of England made substantial improvements to the form in 2004, leading to more robust data from 2003 onwards. For this reason, we have used the Form IPA data from 2003 onwards.

Form IPA collects coupons for fixed rate bonds only. An estimate must therefore be made for variable rate bonds. To do this, the Bank of England has assumed that the average rate of return of variable bonds issued by a particular sector, in a particular quarter, is the same as that for fixed rate bonds. For example, the average rate of return (taken from Form IPA) for MFI-issued fixed rate bonds in Quarter 1 (Jan to Mar) 2011 is used as the rate of return on variable rate MFI bonds issued in that quarter.

The assumptions underpinning this are:

- bonds are assumed to be issued at prices to make investors indifferent between fixed and variable rate bonds, in terms of their expected return

- the implied costs to institutions of issuing fixed and variable rate bonds in the same sector (for example, MFIs) and period (for example, Quarter 1 2011) are assumed to be the same

Once a fixed rate bond has been issued its nominal yield at issue is by definition fixed. Any subsequent changes to the price will not affect the cost to the issuer. Therefore, the implied rate of return in any given year is not a representation of the interest rate or the cost of borrowing in that year. Instead, it represents the cost of existing debt in the economy for that given time period.

The resulting average is termed the “blended rate of return”. Sectors that issue a high proportion of their bonds with fixed rate interest payments therefore require less imputation, and are likely to produce more robust data, than those which issue mainly variable rate bonds. Typically, half of MFI-issued bonds are fixed rate, so the IPA data for this sector are judged a robust point of comparison.

The majority of PNFC-issued bonds are fixed rate. This means that relatively few imputations are required for the PNFC data set. We therefore consider the difference between the PNFC and MFI implied rates of return (using Form IPA data) to be a robust basis for calculating a premium on PNFC-issued bonds. The PNFC premium is calculated for each quarter by subtracting the MFI implied rate of return from the PNFC rate, estimated using Form IPA data. Each quarter, this premium is added to the adjusted MFI rate of return calculated in stage 2. Prior to 2003, the 2003 average premium is used. The resulting premia for PNFCs are shown in Figure 3.

Figure 3: Private non-financial corporations premium on implied monetary financial institutions rates of return, UK 1998 to 2012

Source: Office for National Statistics

Download this chart Figure 3: Private non-financial corporations premium on implied monetary financial institutions rates of return, UK 1998 to 2012

Image .csv .xlsThe other financial institutions (OFI) sector issues mainly variable rate bonds. As discussed, Form IPA does not enable direct estimation of the rate of return on variable rate bonds. This means the OFI dataset is based on a relatively small sample of bonds and can only be used to calculate an approximate premium for OFIs. This means that the OFI implied rate of return tracks the MFI rate closely throughout the time series. Given that many OFIs are special purpose vehicles set up by banks and building societies to issue bonds, this appears to be a reasonable assumption.

Bonds issued by insurance companies and pension funds use the OFI rate. There are not enough bonds issued by these institutions to estimate premiums. As they are a class of financial institution themselves, the OFI rate is a reasonable estimate and the amount of bonds issued by this sector is small, so the choice of premium has little effect on total interest payments.

Bonds issued by non-profit institutions serving households (NPISH) use the PNFC rate, as the pool of NPISH-issued bonds is too small to estimate a separate NPISH premium. Of the three main sectors, NPISH are regarded as being closest to PNFCs in nature and the small quantity of NPISH bonds means the choice of premium has little effect on total bond interest payments.

Direct data are used for public corporations; they are not affected by this change and government bond interest payments are also unaffected.

Stage 4: interest paid by sectors other then MFIs

By the end of stage 3, for those sectors where there are no direct data on bond interest payments, we have derived a quarterly implied rate of return. For each quarter, this rate of return is multiplied by the average nominal value of bonds in issue that quarter to derive the interest paid by that sector. At the end of this stage, the total amount of bond interest paid is known. This therefore will also be the total amount of bond interest received, to be allocated in stage 5.

Stage 5: interest received by monetary financial institutions

Interest received by banks is taken directly from the Bank of England Form PL from 2004 onwards, and Form A3 before then. Building societies are covered by Form PL from 2008 onwards; in earlier years they use the method for other sectors, which is described later in stage 5. The adjustment for manufactured interest derived in stage 2 is subtracted from interest received. This follows the International Monetary Fund (IMF) Handbook on Securities Statistics guidance to treat manufactured interest as negative income.

Other sectors that hold corporate bonds are then allocated the remaining bond interest, based on the proportion of the total remaining bonds they hold. This proportion is calculated quarterly, using the average value of the bonds in the quarter.

In particular, the rest of the world typically holds between 50% and 70% of the remaining bonds. This means that a significant proportion of the increase in corporate bond interest that this change results in is received by the rest of the world. This has implications for both the current account deficit and gross national income (GNI), as discussed in the “Impact of improved methods” section.

Back to table of contents6. Impacts of improved methods

Corporate bond interest

The new method produces estimates of interest paid on corporate bonds that are substantially higher than from the old method, as shown in Figure 4. As discussed earlier in this article, we would expect implied rates of return for corporate bonds to be generally higher than government bonds and this is now the case. At certain points in time (for example, in 2011), the government rate remains higher than other sectors, though short-run differences like this might reasonably come about from timing effects.

Figure 4: New method rates of return on bonds (nominal prices), UK 1998 to 2012

Source: Office for National Statistics

Download this chart Figure 4: New method rates of return on bonds (nominal prices), UK 1998 to 2012

Image .csv .xlsAll of the increase in interest paid comes from UK sectors. Some of the corresponding increase in interest received also goes to UK sectors, but the rest is paid to holders of UK bonds resident abroad. Therefore, this change results in an increase in payments by the UK economy to the rest of the world in the national accounts.

As noted earlier, the numerical impact of these improvements can be found in the Impact of Blue Book 2017 changes on the Sector and Financial Accounts, 1997 to 2012 article, but in summary the current account deficit increases for all years from 1998. It has no impact on estimates of gross domestic product (GDP), as this does not include income from financial investments and assets such as bond interest receipts and the corresponding payments. However, gross national income (GNI) does include such payments and receipts and this change reduces GNI by the same amount as the current account balance.

The changes also affect the net property income received by each UK sector that holds or issues corporate bonds. These changes feed directly through to the net lending and borrowing positions of the sector.

Bond redemptions and net issuance

The impact of the change to corporate bond redemptions is more straightforward. The new method will result in an increase in the value of bond redemptions, causing the value of net bond issuance to be lower. This will make the flow of corporate bond assets (and liabilities) lower than it was previously. This will change the net financial position of several sectors, including private non-financial corporations, other financial institutions and the rest of the world.

Back to table of contents7. Future work

The methods discussed in this article represent considerable improvements to the national accounts. However, the Enhanced Financial Accounts inititative remains in its early stages, and we are continuing to exploring alternate sources and methods across the whole of the National Accounts. Users should continue to expect incremental improvements to all areas of the sector and financial accounts, including to bonds and resulting accrued interest.

Back to table of contents