1. Introduction

This article looks at some of the commercial financial market data providers that we used within the experimental statistics matrix, with examples of additional analysis that use their data, and some of the challenges faced. We focus particularly on Refinitiv, CREST and Equiniti, and Equifax. This article is part of the annual experimental enhanced financial accounts publication.

It is important to emphasise these are experimental statistics which have been produced in isolation of the normal national accounts production and quality assurance process. There are a number of caveats that users of the data should consider.

The data are not consistent with currently published UK financial account statistics, such as the UK Economic Accounts or the Quarterly or Annual National Accounts, for example, and should not be used in place of the regularly published national statistics. The data has been produced outside of current processing of the national accounts and the data will be revised prior to inclusion in any future annual national accounts. We will continue to evaluate and quality assure these experimental statistics and other new data with the aim of incorporating them into the UK National Accounts over the coming years. These experimental estimates may be subject to change as we develop, quality assurance and integrate these data.

Back to table of contents3. Equifax data for short-term and long-term loans to households

We have obtained anonymised borrowing data from the credit reference agency Equifax for consumer loans by “other financial institutions” (UK lenders other than banks, building societies, or insurance companies). This gives us the value of the lending at the end of the period, split between various loan types such as mortgages, credit card debt, and hire purchase.

There are also data on the original maturity of the loans, that is, the time from the loan being originally taken out until the final scheduled payment date. An original maturity of one year or less is classed as short-term lending; an original maturity beyond one year, or with no stated payment date, is classed as long-term lending. Those loans without information on original maturity have been split between short- and long-term loans, in line with the proportions of each in the loans of that type for which the original maturity is known.

The lenders have been sectorised using information from the Inter-Departmental Business Register (IDBR), Companies House and companies’ own websites.

The data from Equifax have enabled us to derive improved data for “other financial institutions” short-term and long-term loans to households. Compared with the existing data, these have greater coverage and are available at a more granular sector level for the lenders.

Back to table of contents4. Supplementary commercial data analysis

This section aims to provide a summary of the impact each source has provided in addition to showcasing examples of additional analysis possible using these data.

Refinitiv

As described previously, the Refinitiv dataset was a primary data source used in the experimental matrix to provide improved estimates of listed shares (AF.511) issued by UK-based (domiciled) companies. The data comprise individual securities listed on stock exchanges across the world, with additional metadata on the type of security (such as ordinary share, preference share option, and so on) and issuer information; with the latter allowing for a more robust domicile concept to be employed, which aligns to the European System of Accounts 2010 (ESA 2010) definition.

The Refinitiv data’s global coverage of exchanges, highly granular (security level) structure coupled with the improved domicile concept has allowed us, for the first time, to accurately capture shares listed by UK-domiciled entities on overseas markets. Overseas markets are defined as any listed stock exchange that is located outside of the UK.

Within the Refinitiv data the value of shares located on UK and overseas markets, at the end of 2017, can be seen in Figure 1. This shows that issues on overseas markets constituted 8% (£193 billion) of the UK listed shares total issuance, at the end of 2017.

Figure 1: Split of UK domiciled company listed shares by market of issuance

Overseas markets provide an uplift of £193 billion at the end of 2017 for UK listed shares

Source: Office for National Statistics using Refinitiv data

Download this chart Figure 1: Split of UK domiciled company listed shares by market of issuance

Image .csv .xlsThe availability of rich metadata has enabled us to provide a further geographical breakdown of (UK-domiciled) overseas share listings. The value each country’s listed exchanges provide, at the end of 2017, as a percentage of the overseas listings total (£193 billion) is presented in Figure 2. It is worth noting that any share listings backed by shares listed on a UK exchange have been removed from the overseas market figures in Figure 2, to avoid double-counting.

Figure 2: United States makes up over 87% of the overseas listed shares market, for UK domiciled entities, at the end of 2017

Overseas markets provide an uplift of £193 billion at the end of 2017 for UK listed shares

Source: Office for National Statistics using Refinitiv data

Notes:

- The other category includes: Switzerland, Cyprus, Sweden, Luxembourg, United Arab Emirates and South Africa.

Download this chart Figure 2: United States makes up over 87% of the overseas listed shares market, for UK domiciled entities, at the end of 2017

Image .csv .xlsFigure 2 shows that the United States contributes over 87% of the overseas total, with Italy contributing around 7%. The remaining countries collectively only contribute less than 6% of the total and include countries such as: Norway, Germany, Canada, France and Denmark.

Equifax

Equifax is one of several credit reference agencies (CRAs) within the UK. All UK companies undertaking lending activities have the option to report this information to a CRA within the UK, although this is not mandatory. However, if they wish to receive “shared data” in order to make credit decisions, it is a requirement to provide data to their preferred CRA. The Steering Committee on Reciprocity (SCOR) set recommendations that suggest lenders should share data with all CRAs. Whilst this is not always the case, most do share with the three main CRAs. Consequently, no individual CRA will have full coverage of total borrowing activities in the UK.

The data received from Equifax are anonymised and aggregated so no individual borrowing information can be identified. It is important to note that we do not have access to any personal information and cannot identify individuals within the data. The data are aggregated by Equifax to geographical level and the type of lending.

Within the experimental matrix, Equifax data have been used to provide estimates on household (consumer) lending for short-term and long-term loans, issued by lenders other than banks and building societies. The household borrowing is aggregated using local authority district (LAD) codes at a unitary authority (UA) level. More information on Equifax can be found in this article.

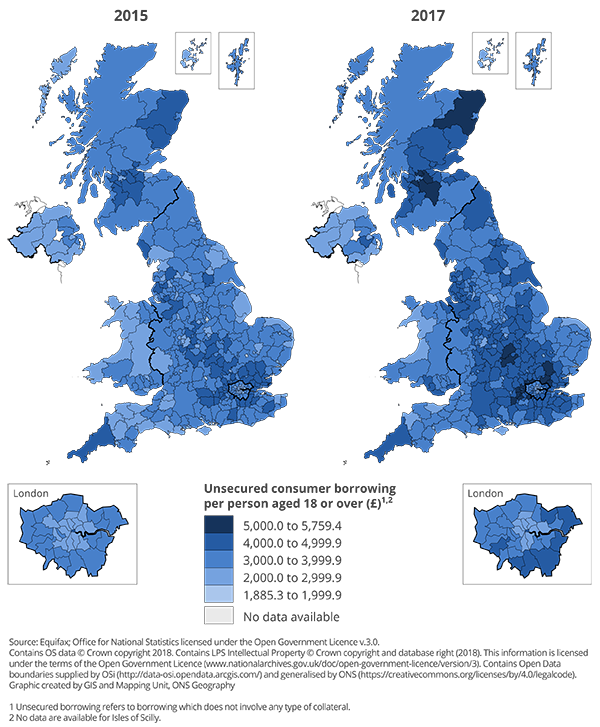

Another example of using data from a commercial source can be found within the previously published Equifax article, where the regional breakdown of lending is visualised in a heat map showing the average amount borrowed by an individual (aged 18 years and over) or company within a given geographical area. These are shown in Annex A within that article and Figure 14 (PNG) of this highlights the spread of unsecured lending by individuals throughout the country, with pockets of higher borrowing in specific areas.

{kind=link}

Commercial challenges and retrospective

The examples in previous sections showcase some of the exciting insights commercially sourced data as a service can provide. However, the relatively new adoption of commercial data for use within the national accounts has provided some unique obstacles to overcome. One of the main challenges has been the interpretation of the definitions underpinning the metadata. This is especially important when adhering to the national accounts framework as the European System of Accounts 2010 (ESA 2010) classifications can share similar naming conventions to categories used by providers of commercially sourced data, but with large variations in the underlying definitions; referred to as conceptual alignment.

An example of an important conceptual alignment issue, for both Equifax and Refinitiv, is in the classification of entities into ESA 2010 compliant sectors. In order to overcome this challenge, we employed the use of other auxiliary data sources to obtain a wider array of metadata. The variables obtained from these sources helped in the formation and validation of the sectorisation methodology employed for Refinitiv and Equifax.

As shown previously, commercially sourced data as a service can be used to provide not only granularity, quality and coverage improvements for areas of the national accounts, but an enhanced insight into other areas of economic interest. However, the replacement or enhancement of existing sources with commercial data for full integration into the UK Financial Accounts does require further development and quality assurance. We will continue to evaluate these existing and other potential commercial data as a service as part of our ongoing commitment to improving the UK Financial Accounts.

Back to table of contents